Corporate 5 Minute Fix 09: financial sector oversight, greenwashing crackdown, ASX Compliance Updates, climate-related financial disclosure

ASIC and AFCA sign MOU to strengthen financial sector oversight

- On 1 December 2023, the Australian Securities and Investments Commission (ASIC) and Australian Financial Complaints Authority (AFCA) signed a memorandum of understanding (MoU) prescribing their ongoing engagement with one another.

- Under the MoU the parties may share, to the extent possible, information relevant to regulated entities or persons.

- This is subject to any statutory secrecy and non-disclosure obligations, other confidentiality and information sharing obligations, or any other constraints, including any imposed by privacy legislation.

The MOU

The MoU promotes AFCA's and ASIC's shared focus on a well-regulated and stable financial services sector to promote consumer confidence. The MoU governs the administrative arrangements between them and acknowledges the intention to collaborate in the exercise of their respective responsibilities.

The parties may also establish supplementary protocols and guidelines to operate under this MoU.

The parties can review the MoU and any supplementary materials periodically and may consult together over the operation of the MoU, where necessary.

Collaboration and information-sharing

The MoU sets out the basis on which ASIC and AFCA will engage.

Each party has agreed to:

- Inform – both parties agree to share relevant information and proactively and promptly respond to information requests.

- Consult – mutual consultation when either considering or undertaking an activity that may impact the other's responsibilities.

- Collaborate – collaborate, particularly in policy development and industry consultation, to improve regulatory outcomes.

- Engage effectively – interactions with each other and with other industry participants, aiming for improved efficiency.

Senior level liaison meetings and other mechanisms will enable sharing of perspectives and expertise on relevant issues.

Any confidential information obtained will not be shared with third parties unless required by law, or in response to a parliamentary committee request or requirement. In such circumstances, each party will advise the other before any proposed disclosure, where possible.

The MoU does not affect any existing statutory obligations applicable to disclosure of information by one party to the other. If the MoU is terminated, any information obtained under the MoU will be treated confidentially.

What to expect

It appears improbable that significant changes will occur as the MoU intends to maintain the ongoing collaboration between ASIC and AFCA. However, it is prudent to note that there might be a more liberal exchange of information concerning regulatory and oversight functions. Therefore, the industry should remain aware of this possibility, even though the MoU provides for strict confidentiality measures.

Background to AFCA and ASIC

ASIC is Australia's corporate, financial markets, financial services and consumer credit regulator. One of its key responsibilities is to regulate the conduct of Australian Financial Services licensees and Australian Credit licensees. It also has some regulatory oversight of the AFCA Scheme under Division 2, Part 7.10A of the Corporations Act 2001.

AFCA is authorised by the Minister for Revenue and Financial Services, and serves as an independent, not-for-profit ombudsman service for the financial services sector.

Its external dispute resolution service helps consumers and small businesses resolve complaints with financial firms in banking and finance, investments and advice, and insurance and superannuation, including those regulated by ASIC. It has obligations under the Corporations Act 2001, its Rules, and its constitution.

AFCA reports to ASIC and other regulators, including in relation to contraventions of the law, systemic issues and the failure to give effect to an AFCA determination.

ASIC continues greenwashing crackdown – Morningstar fined for investments in weapons

The Australian Securities and Investments Commission (ASIC) remains vigilant in its pursuit against greenwashing practices, recently issuing Morningstar Investment Management Australia Limited with two infringement notices totaling A$29,820. These fines result from Morningstar's holdings, albeit for a short period, in securities linked to weapons companies, directly conflicting with its stated Environmental, Social, and Governance (ESG) policy outlined in the Product Disclosure Statement (PDS) of the Morningstar International Shares (Unhedged) Fund, for which Morningstar acted as trustee and responsible entity.

Despite asserting in its ESG policy that the Fund would avoid exposure to stocks affiliated with controversial weapons, as defined by Sustainalytics (Morningstar's ESG research arm), the Fund was found to have held positions in five companies involved in the development or production of nuclear weapons or providing essential components for such arms. These breaches occurred during two short periods in 2022 and 2023.

Morningstar voluntarily reported these incidents to ASIC, prompting the regulatory body to issue infringement notices under the ASIC Act for contravening conduct liable to mislead the public regarding the Fund's nature or characteristics.

These actions against Morningstar mark the latest step in ASIC's ongoing efforts to combat greenwashing within the financial industry, another reminder to industry participants to adhere to their ESG commitments and the importance of transparency in investment practices.

Despite the brevity of the breach, the issue of an infringement notice highlights ASIC's seriousness on greenwashing practices. Yet, proactive self-reporting and open communication with ASIC can strategically benefit an entity, as it demonstrates a clear intent to rectify ESG breaches which may mitigate harsher regulatory actions, like court proceedings, and shape a positive public perception.

Mitigating ASIC scrutiny

We've provided a comprehensive summary of tips to avoid inadvertently falling foul of the law and receiving infringement notices. In essence, ASIC's key message is that companies must be able to provide solid evidence to support their assertions, ESG related or otherwise, and demonstrate their commitment to such claims.

ASX Compliance update no 09/23

AGM observation

After the close of the 2023 AGM season, from September to October, ASX has grouped common issues found during their review of draft notices of meetings (NoMs), as follows:

Description

- Notice of meeting package documents for securityholders should be sent together to ASX for review at the same time and in a single email.

- ASX will only start its review upon receiving all documents. This package includes the proxy form (Listing Rule 14.2) and other necessary documents for securityholders.

- If there's a proposal to change the constitution, provide ASX with a marked-up draft of the amended/new constitution for review (Listing Rule 15.1.1).

- Any missing Appendix 15A or Appendix 15B provisions in the constitution require completion of ASX's constitution checklist alongside the constitution submission to ASX.

- A NoM requiring a voting exclusion statement must align with Listing Rule 14.11; any deviation requires demonstrating to ASX, that the statement has the same effect as the listing rule.

- Irrespective of wording, the entity must exclude all votes mandated for exclusion under Listing Rules.

- Listing Rule 14.1A requires NoMs seeking approval under Listing Rules to outline the relevant Listing Rule and its implications.

- ASX emphasises the importance of correctly determining compliance with placement capacity rules at the time of entering agreements to issue securities under Listing Rules 7.1 and 7.1A.

- The NoM seeking approval for an issue of securities must summarise the agreement's material terms as per Listing Rules 7.3.7, 7.5.7, and 10.13.9.

- ASX noted instances where NoMs omitted agreement details or failed to mention the agreement, ASX recommends entities to explicitly confirm that securities are not being issued under an agreement.

- Entities seeking securityholder approval under Listing Rule 7.1A must include Listing Rule 7.3A information in the NoM.

- Listing Rule 7.3A requires disclosing securities issued under 7.1A in the preceding 12 months and their percentage relating to the total equity securities at the start of the period.

- Common errors noted by the ASX involve the disclosure of all equity securities issued in the prior year instead of specifically those under Listing Rule 7.1A, and failure to include all information required by Listing Rule 7.3A.6 for each issue made under Listing Rule 7.1A e.

- Listing Rule 15.1 requires entities to submit draft documents to ASX before finalisation, and this is applicable when a notice of meeting contains resolutions on constitutional amendments or resolutions seeking approval under the Listing Rules.

- NoMs dealing solely with the Corporations Act matters (eg., tabling of financial statements, director elections) do not require draft submission to ASX; lodgement through ASX Online will suffice for such a NoM.

- Contrary to common misunderstanding, Listing Rule 14.5 does not require providing a draft NoM under Listing Rule 15.1only because it includes a resolution for director election or re-election, as these types of resolutions are not seeking approval under the Listing Rules. re not being issued under an agreement.

Listing Rule 6.23.3 – Prohibitions:

Listing Rule 6.23.3 usually related to any changes affecting an option such as a reduction in exercise price, extension of the exercise period, or increase in the number of securities to be issued on exercise, are not allowed.

ASX has now clarified its position that a performance right that may be exercised by an issue of shares (either by a new share issue or the transfer of existing shares), will be treated as an option under Listing Rule 6.23.3.

The impact of this position is that a board cannot use their discretion to waive performance milestones or hurdles (which are changes that make a hurdle or milestone easier to achieve), or for performance rights to vest on a number of events occurring such early termination of employment as good leaver. These types of changes are now construed as a change that effectively may fall within the prohibition of Listing Rule 6.23.3.

ASX has clarified that it will not consider waivers of Listing Rule 6.23.3 for quoted options, but may consider waivers for unquoted options (performance rights) in limited circumstances, and would allow waivers to obtain shareholders' approval for changes to the terms of performance rights if:

- they are not quoted and were issued under an employee incentive scheme or as remuneration;

- they were issued in compliance with the Listing Rules;

- they represent a relatively small proportion of the entity’s undiluted issued capital (in the absence of other factors, ASX considers this to be less than 5% of the entity’s undiluted issued capital). It is noted that the 5% limit is usually what would be contemplated in an employee share scheme under the terms and conditions of Section 1100V of the Corporations Act; and

- granting the waiver will not undermine any prior securityholder approvals or ASX confirmations that have been given for the purposes of the Listing Rules.

Admittedly it would have been less burdensome for companies, if the requirements for Listing Rule 6.23.3 were carved out to allow changes if the above criteria were met as opposed to apply for a waiver. This may be a topic for further discussion with the ASX.

ASX has confirmed that it will generally not grant waivers if:

- the possibility of any future changes in an option terms and the circumstances where such changes could occur, were not disclosed clearly in notice of meeting approving the issue.

- the option terms were previously disclosed in a prospectus or another disclosure document as part of a Listing Rule 6.1 confirmation.

The ASX also emphasised that disclosure in a notice of meeting of a general power to amend the terms of an option or of a broad discretion to waive the terms of an option does not permit an entity to make changes to an option that are prohibited by Listing Rule 6.23.3.

Cancellation of options

Shareholder approval will be required under Listing Rule 6.23. for any changes that effectively cancel an option for consideration. The note to Listing Rule 6.23.2 highlights that cancelling an option in consideration of a new option might be prohibited under Listing Rule 6.23.3 if it impacts exercise price, exercise period, or securities received on exercise.

A change that has the effect of cancelling an option in consideration of the issue of a new option may only be allowed if:

- cancellation of the original option is not conditional on the issue of the new option and shareholder approval under Listing Rule 6.23.3 is obtained; or

- the entity obtains shareholder approval under Listing Rules 6.23.2 and 6.23.4 for the change, after a waiver from Rule 6.23.3 is granted.

Going forward, boards should be mindful when designing remuneration packages bearing in mind the lack of flexibility to the change of terms of options and performance rights, such as the milestones and events for early vesting.

ASX Compliance Update 01/24

As of 5 February 2024, Entities must comply with new procedures when applying for admission to the Australian Securities Exchange (ASX).

The changes aim to increase compliance with the existing listing rules.

Spread requirement

Spread register template

Entities must now use the new ASX spread register template to submit details of security holders who are intended to be counted for spread. No other format will be accepted.

Attestation

Applicants must now submit an attestation of compliance with the "spread requirement" in Listing Rule 1.1, Condition 8, from the principal of a law firm acting for them confirming the lawyer has:

- read and understood Listing Rule 1.1 Condition 8 and Guidance Note 1 (in particular section 3.9 and its footnotes);

- reviewed the information provided in support of the minimum spread requirement; and

- taken reasonable steps to confirm that the security holders presented are able to be counted for spread in accordance with ASX’s Listing Rules and guidance.

An attestation confirming that the entity has 600 or more non-affiliated security holders provides an exception to the spread register template requirement, unless a template is subsequently requested by ASX.

Escrow documentation

The ASX Restricted Securities Table has been updated. Where an entity has or will have restricted securities on issue at listing, this table must be submitted with an Appendix 1A Listing Application.

An entity must give an Appendix 9C restriction notice to a holder in all circumstances where the holder is subject to ASX-imposed escrow. This replaces the general requirement for listing applicants to use restriction deeds, unless ASX directs otherwise.

Material contracts

An entity submitting an Appendix 1A Listing Application will not have to submit all material contracts referenced in the Offer Document.

Material contracts are now only required where the contract relates to the securities to be quoted, or completion of the contract is a condition of the Offer. ASX may request copies of other contracts referenced in the Offer Document if it considers necessary.

Communication person

A reminder that Listing Rule 12.6 requires an entity to appoint and maintain a person responsible for correspondence with ASX in accordance with section 4.9 of Guidance Note 8. New nominated contacts must pass a free compliance course before appointment as "Communication Person" through ASX Online.

Updated forms and fees

Updated ASX appendix forms are now available online and must be used going forward.

Additionally, ASX has made changes to Guidance Note 15 and listing fees. This includes a change from a flat fee for the quotation of additional securities to a fee of 1.5% and associated changes to billing calculations. ASX also plans to introduce monthly billing in the near future.

Draft legislation on climate-related financial disclosure

On 12 January 2024, the Australian Government released a draft legislation seeking to amend parts of the Australian Securities and Investment Commission Act 2001 (ASIC Act) and Corporations Act 2001 (Cth) in a commitment to improve the quality of climate-related financial disclosure and providing Australians and investors with greater transparency about climate-related financial risks, opportunities, plans and strategies.

The Government's goal is to improve climate disclosures to support regulators in assessing and managing systemic risks to the financial system as a result of climate change and efforts to mitigate its effects.

The new amendments showcase new climate-related financial reporting requirements for entities aligned with the current financial reporting regime under Chapter 2M of the Corporations Act. Specifically, it includes a new "sustainability report" requirement in addition to the current financial statement requirement for entities.

Who must complete the reporting?

The Government has identified the following as reporting entities:

- large entities (defined in section 45A of the Corporations Act) that must prepare and lodge annual reports under Chapter 2M of the Corporations Act;

- large asset owners (asset owners will be considered large if funds under management are more than AU$5 billion; and

- entities subject to annual reporting requirements under the Corporations Act and National Greenhouse and Energy Reporting Act 2007 (NGER Act), regardless of the size.

Phasing

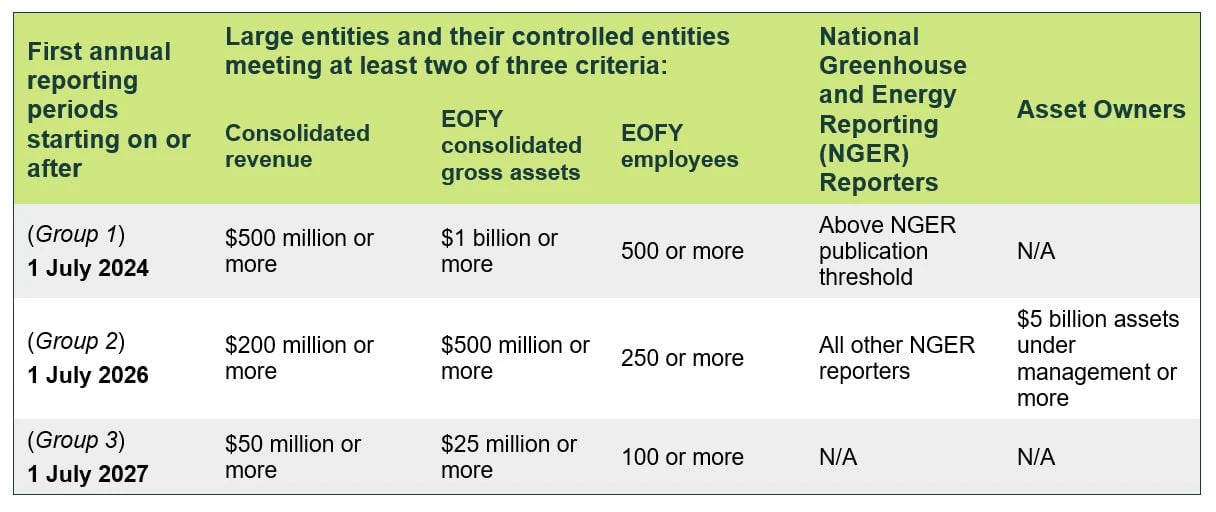

The reporting entities will be phased out in three groups, over a four-year period based on size or level of emissions.

The table below sets out when entities must commence mandatory disclosure:

At present, the commencement date for Group 1 is July 2024. However, the Government is welcoming stakeholder feedback whether amending the legislation to require a 1 January 2025 commencement date instead would improve the quality of reporting during the transition year.

Exemptions

The following entities are exempted under the draft legislation:

- small and medium entities; and

- entities registered within the Australian Charities and Not-for-profits Commission.

Notably, entities which fall within Group 3 and have no material climate-risks or opportunities are only required to disclose a statement to that effect.

Reporting content

The climate-related financial disclosures must include the following information about an entity's climate-related risks and opportunities, as required by Australian climate disclosure standards:

- information relating to governance, strategy, risk management and metrics and targets. This includes Scope 1 (direct emissions generated by operations) and Scope 2 (indirect emissions from energy-purchased and used) greenhouse gas emissions within the first year of reporting; and

- Scope 3 (indirect emissions along the wider value-chain) which will be required from the second year of reporting.

Furthermore, the sustainability report is expected to consist of:

- climate statements prepared in line with the relevant sustainability standards issued by the Australian Accounting Standards Board;

- notes to the climate statement inclusive of disclosures as legislatively required, and notes by the sustainability standard if any;

- any statements prescribed by the regulations for the year; and

- the directors' declaration about the compliance of the statements with the relevant sustainability standards.

Reporting framework

The climate-related financial disclosure will sit within a sustainability report and become a part of the reporting entity's annual report. The timing of the annual report lodgement will be consistent with the requirements under section 319 of the Corporations Act.

Assurance requirements

The disclosure will be subject to similar assurance requirements for financial reports per the Corporations Act. Entities will be required to obtain an assurance report from their financial auditors, who will use technical climate and sustainability experts where required. The Australian Auditing and Assurance Board will develop assurance standards in line with the International Auditing and Assurance Standards Board's final standard.

Liability framework

The climate-related financial disclosures will be subject to the existing liability framework under the Corporations Act, and ASIC Act.

Modified liability

For the reports issued between 1 July 2025-30 June 2028, only the regulator will be able to bring action relating to breaches of relevant provisions made in disclosures of Scope 3 emissions and climate-related forward-looking statements. Furthermore, the only remedies available to the regulator are injunctions and declarations.

More details are available in our article Draft legislation released for mandatory climate reporting framework.