Jennifer Ball

Partner •

Sydney

Stakeholders have until 11 May 2018 to comment on a key part of the new ipso facto regime – the exceptions to the statutory stay on ipso facto clauses in certain categories of contracts and rights.

The new insolvency legislation commencing 1 July 2018 (Treasury Laws Amendment (2017 Enterprise Incentives No. 2) Act 2017) introduces a statutory stay on the exercise of contractual rights arising by reason of certain insolvency trigger events.

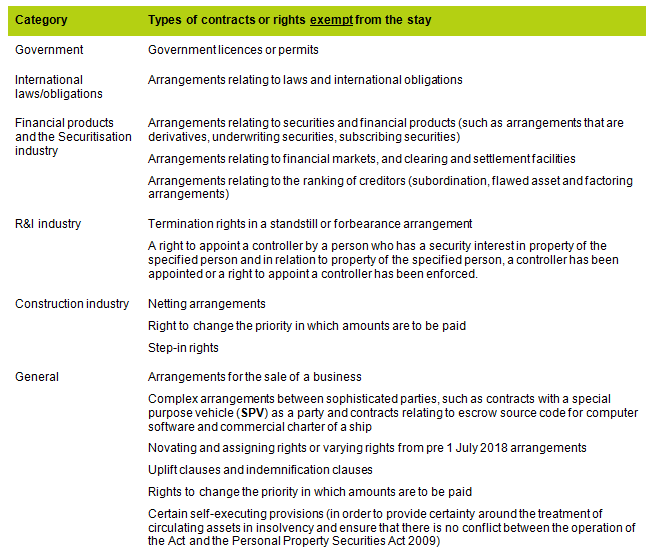

Treasury's Exposure Draft of the Corporations Amendment (Stay on Enforcing Certain Rights) Regulations 2018 and the Corporations (Stay on Enforcing Certain Rights) Declaration 2018 propose exemptions in the following categories:

Key issues for stakeholders to consider

Interestingly, the proposed exemptions are much broader than previously contemplated in the exposure draft for the Act and in its Explanatory Memorandum. The breadth and nature of these proposed exceptions are likely the result of further consultation by Treasury with specific industry groups, particularly in relation to the construction and banking and finance sectors (for example, exceptions relating to the use of special purpose vehicles, arrangements for the sale of a business and step-in rights).

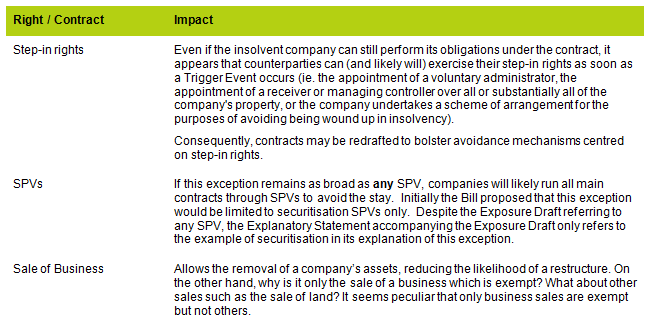

For many stakeholders, these proposed exemptions will be welcomed. However, the breadth of the proposed exceptions now likely creates some doubt as to whether the Act will be able to meet its stated objective of promoting and facilitating the restructuring of distressed businesses in Australia, particularly where the exceptions permit a counterparty to remove or take control of assets from the distressed company, making it more difficult to implement a successful restructure.

For example:

Many of these issues will need to be worked through by Treasury before the regulations are finalised. We will be exploring the scope and practical effect of the proposed exemptions in future articles, including on the final version after the official release on 1 July 2018, explaining the exemptions and how they will likely operate in practice.