Stuart MacGregor

Partner •

Brisbane

The 2024 Hydrogen Strategy sets out the vision for hydrogen in Australia, which is for a “clean, innovative, safe and competitive hydrogen industry that benefits Australia’s communities and economy, enables our net zero transition, and positions us as a global hydrogen leader”.

On 13 September, Minister for Climate Change and Energy Chris Bowen launched the Australian Government’s 2024 National Hydrogen Strategy. The strategy aims to provide the framework to position Australia as a global hydrogen leader by 2030. The Government has indicated that it hopes the Strategy will be a “blueprint for Australia to develop new domestic clean energy manufacturing capabilities and capitalise on massive export opportunities for clean, secure energy supply chains through becoming a hydrogen world leader”.

The Australian Government is extremely upbeat about the possibilities for the development of the hydrogen market for domestic uses and international trade. This position is well encapsulated in the market summary set out on the website of the Department of Climate Change, Energy, the Environment and Water, which is worth setting out in its entirety:

“Australia has an ambition to be a global hydrogen leader. Alongside renewable electricity, hydrogen will play a significant role in decarbonising our economy. It will support the export of hydrogen embodied locally manufactured products.

We can use hydrogen:

The global hydrogen market has been forecast to reach US$1.4 trillion in 2050. Australia has a range of comparative advantages in this market. These include vast renewable energy resources, space and land. These advantages allow us to competitively manufacture clean hydrogen and its derivative products for our own use, and to supply the world.

Australia has the largest pipeline of hydrogen projects of any country in the world. It has an estimated value over $225 billion. There are more green hydrogen projects under development in Australia than in any other country.

Hydrogen is central to the Australian Government’s vision for a Future Made in Australia. There is an opportunity to grow the Australian hydrogen industry sector. This will capture the significant economic, trade, export and investment opportunities that are becoming available.”

The previous hydrogen strategy (2019) was subject to a formal review process, including public consultation, which closed in August 2013. While Australia’s initial strategy was among the first national hydrogen strategies announced globally, more than 30 countries followed suit, and investment in hydrogen development projects in other countries (reaching Final Investment Decision) started to outstrip the development of comparable projects in Australia.

In addition, as noted in the National Hydrogen Strategy review – Consultation Paper, notwithstanding Australia’s position as an early mover in the hydrogen sector and with considerable natural advantages, “the creation of new, extensive policy measures in other countries to support the development of their domestic hydrogen industries ... [including the] Inflation Reduction Act in the US … which provid[es] tradeable tax credits for hydrogen production that can be combined with tax credits for related renewable energy production and end use cases.” It further noted that a “number of large economies have responded with similar, albeit not quite as extensive, support mechanisms.”

The consultation process therefore posed the following questions:

The Strategy sets out the vision for hydrogen in Australia, which is for a “clean, innovative, safe and competitive hydrogen industry that benefits Australia’s communities and economy, enables our net zero transition, and positions us as a global hydrogen leader”.

The first four chapters of the Strategy outlines four objectives that focus new and ongoing Government policy decisions:

Key among the policy initiatives are the following, which are focused on Objective 1. Some are newly announced, and others are existing policy announcements or funding arrangements:

In addition to these major policy initiatives, a focus on strengthened approvals processes, infrastructure planning and workforce development, skills and training round out the initiatives for Objective 1.

Objective 2 will focus on demand and sector prospects, including green metals (iron and alumina), ammonia, long-haul transport (road, aviation and shipping), power generation and grid support, all linked by the Government’s existing Safeguard Mechanism which incentives large industrials to decarbonise.

Objective 3 emphasises benefit sharing and availability with First Nations communities, regional jobs and businesses, together with the intention to plan for sustainable water use, the adoption of voluntary hydrogen industry codes of conduct for community engagement and partnerships to encourage best practice, and the promotion of best practices by the independent Australian Energy Infrastructure Commissioner.

Objective 4, building on existing bilateral and multilateral arrangements, aims to capture a share of international hydrogen markets through attracting investment and partnerships, developing a Guarantee of Origin scheme in line with international developments, and securing effective international supply chains to support project and market development. Australia already has bilateral clean energy or hydrogen arrangements with Japan, the Republic of Korea, the United States, Germany, Singapore, India, the United Kingdom, the Netherlands and Denmark. Australia is also a participant in several multilateral for a and organisations focussing on hydrogen, including the Mission Innovation Clean Hydrogen Mission, the Clean Energy Ministerial Hydrogen Initiative, the QUAD Clean Hydrogen Partnership, the Indo-Pacific Economic Framework Clean Economy Agreement and the International Partnership for Hydrogen and Fuel Cells in the Economy.

A substantial part of the Strategy is dedicated to outlining existing and proposed future collaboration between Australian Governments. In addition to several detailed project and hub development summaries for all States and Territories, the Strategy identifies the following areas of ongoing focus:

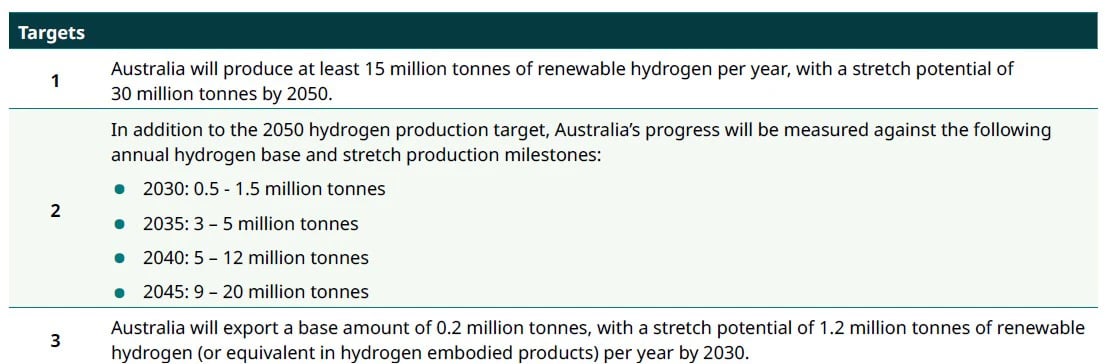

The Strategy summarises three major hydrogen production targets (as noted above) and 34 actions (in five categories, being the four Objectives plus a review and reporting category).

The full list of targets and actions is summarised in Appendix A of the Strategy, and these are given detailed treatment in Chapters 2 to 6.

In relation to Targets, the Strategy provides the following:

While all the proposed Actions are important, from a legal perspective regarding hydrogen development projects and the future of the hydrogen market, the following 10 actions are likely to be particularly noteworthy for potential investors:

Consistent with Actions 29 and 21, the 2024 Strategy has been released with translations into Korean and Japanese. In light of the existing bilateral agreements to which Australia is party, this gives a significant indication of the Government’s focus for development partnerships and investment into the Australian hydrogen sector.

Our next Insight article will summarise the GO bills noted above.